Affordable life insurance in Canada means getting the right amount of coverage for your needs at a price that is fair. The lowest premium is not always the best choice, because too little coverage can leave your loved ones short later.

The goal is to protect your income, debts, and future plans while keeping the cost manageable. This guide will help you understand what affordable really means, compare your options across insurers, and find good value without underinsuring.

Life insurance can seem confusing, but the main idea is simple. An affordable life insurance plan is an insurance policy that gives you good protection, and the premiums stay low enough for your budget each month.

In Canada, many people begin with term coverage. This is because it is easy to get and costs less than other types. You will see different prices from brands like Canada Life and more, so it is important to know what you get for your money before you compare quotes.

Affordable life insurance is coverage you can get and keep without putting stress on your money. A low price can help, but the real question is if the plan works for what you need and if you still pay for it each year without trouble.

There are a lot of things that change insurance rates and how much you pay for your plan in Canada. The biggest ones are your age, if you are male or female at birth, health history, if you smoke, your way of living, your job, your hobbies, how much coverage amount you want, and what kind of life insurance policy you get. Insurance companies use their own ways to figure out prices, so one person can look at two places and get two very different prices.

This is why affordable life insurance is not the same for all people. For example, if you are young, do not smoke, and have good health, you may get a very low cost for your plan. If you are older, have some health conditions, or use tobacco, you can still get a good price. You may just need to pick the right coverage amount, number of years, and insurance company.

The right affordable policy helps cover your real financial needs. If you have a family in Canada, this can mean taking care of income, paying off debts, and saving for your children’s education. If you get a cheap plan that does not do enough, you can have a bigger problem later.

Start by thinking about what your family will need if you are not there. You have to look at things like mortgage payments, credit cards, child care, and daily bills. These should be more important to you than picking the insurance coverage with the lowest price. The right coverage amount should fit your timeline and what you have to pay or handle.

Be sure you look for these coverage options when picking insurance:

Life insurance gets a lot easier when you know some basic words. Term life insurance gives you coverage for a set time, like 10, 20, or 30 years. If you die during these years, your loved ones will get the death benefit.

Permanent coverage stays active for your whole life. Some of these plans can also build up something called cash value. Because you get lifetime coverage and extra features, the price is often higher. For many Canadians, term life is the most affordable choice. It helps protect you and your family during the years you need it most.

Here are some important words you should know:

Canadians often need to pick from three main choices. These are term life insurance, permanent life insurance, and no-medical choices. Each type of life insurance policy has its own reason for being used. Every insurance policy like this also has its own cost.

Most people who want to get good insurance coverage at a low price will look at term life. This is often the first choice for many. Permanent life insurance works well if you want to take care of final expenses or for estate planning. If you find it hard to get through the usual process, no-medical plans can help. In the next parts below, you can see how these types of insurance coverage compare when it comes to cost and what you get for your money.

Term life insurance gives you a set time of coverage. You choose how long you want, like 10, 20, or 30 years. You pay the cost every month or year. If you die while the policy is active, your beneficiary gets the money.

Term life is often the best low cost choice in Canada. It can help you with things that you only need for a time, such as term length for a home loan, money for children’s education, or help replacing your income if something happens to you. There is no cash value, so you do not pay for extra features you may not use.

The price you pay depends on how long the insurance lasts, your age, health, and how much you want for coverage amount. Shorter terms most times have lower costs. That makes term life insurance a good way to get strong coverage now for a price you can handle. It is a big part of many life insurance plans and often searched for as family life insurance Canada.

Permanent life insurance gives you coverage for your whole life, not just for a few years. This type of life insurance includes whole life, universal life, and term to 100 options. Because this insurance lasts your entire lifetime, you will often pay higher premiums.

But it can be good for people who want a small and lasting plan, like to cover funeral costs or end-of-life bills. People who look up “term to 100 life insurance Canada” usually want this kind of simple permanent life insurance. It gives protection for life without extra add-ons that cost more.

The price still depends on your age, health, if you smoke, and how much coverage you need. Universal life insurance is lifetime coverage, but it gives you an extra way to invest money. But that added part and the cost mean universal life may not be the best choice for people who mostly want lower premiums. This kind of life insurance can also help with estate planning.

For most people, term life gives you better value for a short or medium time. You get a higher coverage amount for less money. That is because the life insurance company covers you only for a set number of years. This is why when people look at term life and whole life insurance in Canada, they often pick term life for its lower cost.

Permanent insurance gives you lifetime coverage. It can also grow a cash value. But you pay much more each month for this. If you want to replace your income or cover debt while your family counts on you, term life usually is the better choice.

A quick value check:

Yes, some insurers in Canada sell no medical life insurance and simplified issue life insurance plans. You can get these plans if you have some health problems, need fast approval, or have been told no for regular coverage in the past.

Simplified issue life insurance often asks just a few medical questions. Guaranteed issue life insurance is open to everyone, but this one should be your last choice. It costs a lot more and sometimes there is a waiting time before you can get the full payout if the death is not from an accident.

Here are some things to think about:

Many providers in Canada give these choices. But if you can get coverage through the usual process with more medical questions, you often get a much better deal.

The cost of life insurance in Canada depends on the kind you want to buy and who you are to the risk. Insurance premiums for a healthy person who is 18 can start very low. If you get the same coverage amount later, you pay a lot more.

Still, looking at averages can help. This gives people an idea of what the monthly premiums could be. The cost changes by age, coverage amount, and policy type. The numbers below are true examples from the Canadian market. They show why it is good to compare quotes before you pick any company, even one like Canada Life.

Age is one of the biggest drivers of monthly premiums. In general, the younger you apply, the lower your insurance rates. A healthy applicant in their 20s or 30s can often lock in far lower pricing than someone applying in their 50s or 60s.

Illustrative 10-year term rates for $500,000 of coverage show the pattern clearly. Province can affect pricing, but age usually has the stronger effect. Differences between provinces exist, yet they are often smaller than the pricing jump caused by waiting another decade.

These are sample rates for healthy non-smokers. Your quote may vary by insurer, province, and underwriting result.

The amount of coverage you pick changes your life insurance premiums. If you want more protection, your payout can be higher. That means your premiums will go up when you add more insurance coverage. The rise in cost is not always 1-to-1, but there is still a pretty big increase.

Let’s look at the market to see how this works. There is a 10-year term policy for $100,000. It can start at only $6.29 a month for a young person in good health. If you double the coverage amount to $200,000, the premium goes up to $9.17 a month. So, picking the right amount of life insurance coverage is important.

If you want to compare quotes well:

This way, you find the best value for what you get. It is not just about getting the lowest price.

The type of policy you pick can change how much you pay. Term life is often the least expensive choice. It gives you protection for a certain time. Permanent coverage usually costs more because it lasts your whole life and can have some extra features added in.

There is a big difference in prices in Canada. For an 18-year-old female non-smoker in Ontario, you can get term life coverage for $100,000 starting at about $6.29 each month. If you go for a low-cost permanent coverage, $25,000 starts at about $14.18 each month. So, you pay more for permanent coverage and often get less amount in coverage.

This is why term life is a better pick if you want to save money. When your needs only last for a few years, maybe for things like income or a mortgage, the kind of policy you choose can really help you keep your costs low.

Rates can be different across provinces, but not always by a lot. Most people think insurance rates change more than they do, but that's often not true. When companies set insurance rates, they do look at where you live, so you will need to say your province when you use an online quote tool.

But province is just one of the things insurance companies look at. Your age, sex at birth, if you smoke, your health, and the coverage amount will have more effect on what you pay. Where you live, like being in Ontario, Alberta, or British Columbia, does matter, but it’s not all that matters.

Because of this, it is smart to check out quotes from different companies. Do not always think Canada Life or any one brand is the cheapest in your area. Check a few companies at the same time so you get the best idea of value for your needs.

The most affordable life insurance options you can get right now are usually term policies that are fully underwritten. These are the best life insurance value because they are priced for your situation, not just a guess or for extra things that are not sure.

But this does not mean that one product is right for everyone. There are young adults, families, freelancers, and seniors. They all want different things from their life insurance. The best life insurance is the one that matches your risk and is a price you can keep paying. Let’s take a look at some practical life insurance options for each stage of your life.

Yes, young adults in Canada often find it easy to get low-cost life insurance. If you are young and in good health, term coverage is often very cheap. Many people can get this coverage by going through a simple digital application process.

This time in your life is a good time to get life insurance. The reason is that the price of coverage goes up as you get older. If you are searching for life insurance for young adults in Canada or wondering when to buy life insurance, it is better to buy it now instead of waiting. This is more true if you think you will have a family or have to pay off debts in the future.

Smart ways to start include:

With early action, young buyers can lock in good life insurance coverage and keep their payments low year after year.

Families often need life insurance for things like covering lost income, paying for a place to live, and taking care of children’s education. So, when you look for an affordable life insurance policy for your household, you should think about what your family needs first and how much the premium will be second.

Term coverage can be the best choice for family life insurance in Canada. It is often less money, so parents can get a bigger payout at a lower price during the time their kids need them most. Some insurance companies also have helpful extras, like free child coverage or a discount for couples in the first year.

When you compare your choices, look at these things:

Many people who want life insurance for parents in Canada begin with these things in mind.

If you are self-employed, it helps to have flexible insurance options. Your income may not be the same all year, and every year can be different. The right insurance coverage can protect your family without making you use too much of your money for high costs.

Term insurance is often a good pick. It costs less and can line up with your business loans or your family needs. People who search for affordable business insurance Canada, business insurance for entrepreneurs Canada, or business overhead insurance Canada may need other advice. This is because your personal life cover and your business risk cover help you in different ways.

Useful ideas include:

Keep your personal needs and business needs clear. This will help you not pay more than you should for the wrong policy.

For seniors, the most affordable life insurance options are smaller term policies or simple permanent coverage made for final expenses. Prices go up as you get older, so people often choose coverage that gets the main job done instead of going for big policy amounts.

For example, a 60-year-old woman who does not smoke and lives in Ontario could get a $50,000 term policy starting at about $20.01 each month. If she wants permanent coverage for the same amount, it could cost $100 a month or more. That is a big difference. This is why term coverage is also still important for many seniors.

Common affordable life insurance paths include:

For many seniors, the best value comes from only looking at the real reason why you want coverage.

Term life insurance is often the lowest-priced way to get life insurance. This is because it lasts for a set amount of time and does not have any cash value. This setup helps keep the costs down. It also lets you get a good death benefit without paying a lot.

If you want affordable life insurance, this can be the best option. You may get much more coverage for lower premiums than with permanent insurance. The points below show how things like term length, how simple it is, and real quotes from the market make term life insurance the top low-cost choice.

The length of your term life insurance policy can change how much you pay. If you pick a longer promise from the company, it will usually cost more. For example, a 10-year term life insurance policy is often much cheaper than a 20-year or 30-year term life insurance policy when you want the same coverage amount.

But, picking the cheapest term is not always best for you. If you have a mortgage that will last 20 years or you have young children, a longer term life insurance policy can give you better value. It keeps you and your family safe during the time you need it most. The key is to match the term length to what you have to take care of.

Insurance premiums often go up as you get older. So, if you buy life insurance early and pick the right term, you can save money. If you wait too long and renew later, the price for a new life insurance policy might be much higher than if you had acted sooner.

Term policies are simple to understand. You choose your life insurance coverage, set the term, and pick who gets the money if something happens to you. You just pay your premium. There is no need to look at cash value, think about investments, or deal with complex insurance plans.

This easy setup can also make the cost lower. With a term policy, you get a product that is simple and has fewer extra costs. The application process stays smooth and quick. For most families, simple life insurance is just what they want.

Why buyers like term:

If you want to see life insurance explained Canada in plain words, term policies are often the best way to start.

Term may be better than permanent insurance when you need to cover big risks for a short time. If you want financial protection while your kids still count on you, or while your home loan is high, then term coverage often fits well.

Permanent insurance is good for long-term needs, like covering final expenses or helping with estate planning. Still, the cost can take away money from other things you want to do, like saving or paying bills. This is a big thing to think of for younger families who work to balance their insurance, savings, and regular spending.

Term often works best when you need:

For many homes, this makes term the smarter choice.

Sample quotes show why comparing insurance companies is so useful. Even for the same type of term life insurance, monthly premiums can differ from one insurer to the next.

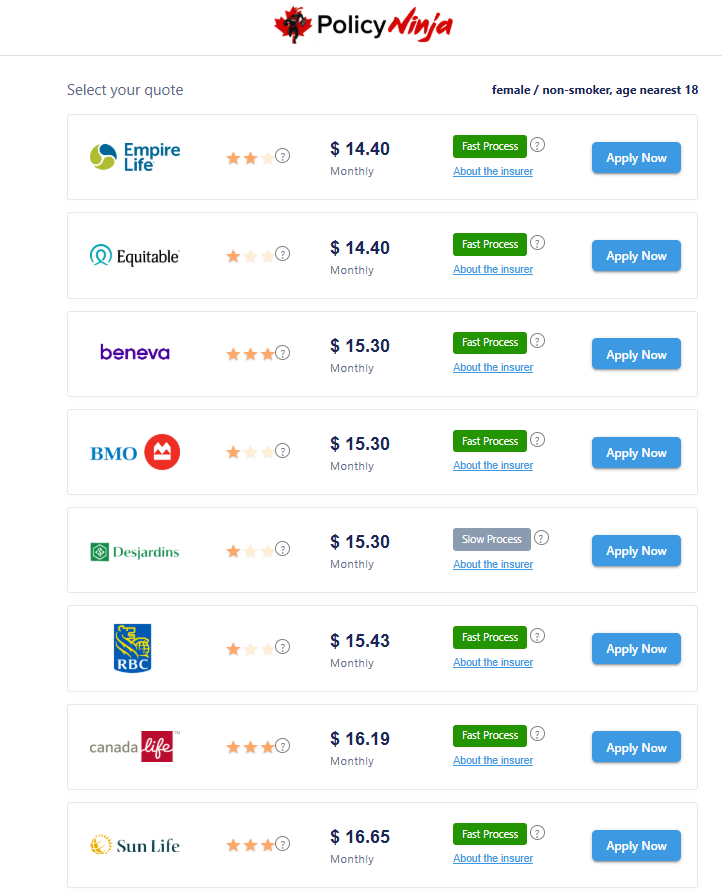

Here is an example for $100,000 in coverage for an 18-year-old female non-smoker living in Ontario:

The cheapest rate is not always enough on its own. Check policy details, underwriting approach, and any useful built-in features before deciding.

Life insurance premiums are set during the underwriting part of the process. Insurance companies look at how likely and how soon they think a claim could happen by checking the risk in your application. This is how they decide what your insurance rates will be.

Some things, like age or family history, stay the same. Other things, like if you smoke, your weight, or some health conditions, can change as time goes on. When you get what makes life insurance premiums go up or down, you can shop for a good policy. This can also help you make it more affordable.

Age is one of the big things that can change the price of any life insurance policy. If you get life insurance when you are young, your insurance premiums will be lower. This is because companies see younger people as having less chance of dying soon.

The gap in price can be big. For example, data shows the cost for a term life insurance policy is about $10.35 each month for an 18-year-old. For a 70-year-old, the price jumps up to $163.37 a month. The exact price will be different depending on the insurance company, but the pattern stays the same.

This shows why the timing of a life insurance policy matters a lot. If you buy life insurance early, you pay less and get more to pick from. If you wait, your costs will be higher. You might not get as many options, and if your health gets worse as you get older, companies will check more things before giving you a policy.

Your health can change the price you pay for life insurance. People who are in good health often get lower insurance premiums. This is because the insurance company thinks they are less of a risk right now. The company will look at things like your height, your weight, past health problems, and what treatment you have had in the past.

The way you live is also important. The company might ask if you drink alcohol, take part in risky sports, or work at jobs like mining or logging. If you have a safer way of living, you could get a better price. Sometimes, if your health gets better later, you can ask the company to look at your rates again.

People with health conditions should look at fully underwritten medical life insurance first. This kind of coverage can still cost much less than plans with no medical checks, even if you have a medical history. That is good to know for anybody who wants to compare life insurance options.

Smoking really affects insurance rates a lot. In Canada, if you smoke, you will often pay much more for it than people who do not. The price difference gets even bigger as you get older. Many products can count, including tobacco, vaping, chewing tobacco, nicotine gum, patches, and other types of nicotine.

On average, smokers spend about 69.59% more on insurance rates when we look at all the data. For people who are older, the numbers go up even more. This is one of the clearest reasons why your premium gets higher.

Important points:

If you do smoke, it helps to compare different insurers because prices can be very different from one to another.

You need to pick a coverage amount for your life insurance that will protect the people who count on you. Most of the time, this means you should think about your debts, how much money your loved ones would need if you are not there, and things you pay for in the future, such as children’s education. If you buy way too much coverage, the policy might be too pricey for you.

A life insurance calculator can help you guess the right insurance coverage you need. It lets you think about your mortgage, any loans you have, your pay, and what your family spends each month. This helps you get a smarter number instead of just guessing or picking an amount because it feels cheap or sounds normal.

A quick coverage check should have:

Affordable insurance coverage is when the plan protects your family but is still okay for you to pay for.

A shorter plan often costs less each month. This can make you want to pick the lowest price you see. But getting affordable life insurance is not just about the cost. You should also think about how the term length fits your needs.

If you have kids who are only five years old, picking a 10-year policy may not be right. Your coverage could end before your kids can get money on their own. In this case, a 20-year plan might be better. The price is higher, but it covers a longer time when you need protection most.

There is always a give and take in life insurance. A fair price is important, but making sure it helps you when it should is more important. Try to pick a term length that follows your needs and plans, and not just the cheapest rate today.

Low-cost life insurance comes with a few things you often see. If you look for Canadian life insurance, you will find fast online forms, simple term plans, and just a few extra options. This helps keep the price low.

This can work well. Simple life insurance plans make it easy to check other options and pay less as time goes by. Even so, it is good to know which parts of life insurance give value and which parts make the price go up without much help for you.

Many insurers in Canada now offer faster underwriting. This means the application process does not take as long. Some people may not need to take a medical exam but can still get coverage that is checked well.

This helps if you want to get approved fast but do not want to pay more for a no-medical plan. You still have to answer medical questions, but the company might look at digital records or other background info instead of making you go for an exam.

Common benefits include:

For people watching their money, this can make things easier. It helps you apply and answer medical questions without raising your payments right away.

Level premiums do not go up during your term. Renewable premiums can get higher when you renew the policy, especially if you renew each year after the first term ends. This is what makes a big change in how much you will pay in the long run.

Most term policies have a set price for the start, so it is easy to plan. If you keep the policy after that time and do not get a new one, the new cost might jump a lot because you are now older.

When you look at insurance rates, make sure you ask:

A low starting price is good, but you want to know how this price may change over time, too.

The keywords included are insurance rates and term policies.

Riders are extra options you can add to an insurance policy. Some riders can help, but each one will make your cost go up. If you want affordable life insurance, it is smart to have riders that you need and that do something good for you.

Most people do not need a lot of extras. The basic things, like the ability to change or renew your policy, are built into many term plans. So, paying more for things that are already there might not be worth it. Families need to look at what will fix a real problem.

A low-cost way of thinking about riders is:

This idea helps keep the value of your insurance policy while making sure you still get the protection you want. This way, you have affordable life insurance that works.

No medical life insurance can help when it's hard to get approved by the usual way or you need life insurance fast. In Canada, this includes plans called simplified issue life insurance and guaranteed issue life insurance.

These types of life insurance are easy to get, but they are not always cheap. The price is often much higher than other life insurance plans, and the payout may be lower. It’s good to know when it’s better to go with the easy choice, and when you should stick with a regular plan.

No medical life insurance is a good option if you need to get coverage and the usual review of your health will not work well for you. This can be the case if you have health conditions, want an easy application process, or have been turned down before.

It can be helpful when time is short. Some people want less steps and a faster answer, often as they get older. Simplified issue life insurance is often a better first pick for no medical life insurance. It will still ask a few health questions, but it often costs less than guaranteed issue.

This plan may be right if:

It can be a good backup to help you get insurance, even if it is not always the lowest cost plan.

The main problem with no medical life insurance is the cost. You often have to pay higher premiums for this type of life insurance because the company doesn't get a full look at your health before they approve you.

You may also get less coverage than you would with other plans. Some guaranteed issue policies can come with waiting periods for deaths that are not accidental. A simplified issue can be cheaper than a guaranteed issue, but you still end up paying more than you would for regular coverage that needs a full health check.

Watch out for these things:

That's why a lot of people who know about life insurance say it’s best to try for regular fully underwritten coverage if you can.

Yes, there are many insurance companies in Canada that give no-medical or easy-to-get coverage. The most popular choices are Canada Protection Plan, Sun Life, Empire Life, Manulife, Beneva, UV Insurance, Humania Assurance, and some others.

The best insurance company for you will depend on your age. It also depends on how healthy you are, the coverage amount you want, and if you want simplified issue or guaranteed issue. Each company has its own way of doing things, so what works well for one person may not work for another.

When you look at different insurance companies, check:

A comparison service and help from someone with a license can make this much faster and easier.

You can get no medical life insurance in Canada, but it is usually not cheap compared with fully underwritten coverage. The convenience and easier access come with meaningfully higher insurance premiums.

Sample monthly premiums for a 60-year-old female non-smoker in Ontario with $50,000 coverage show the difference:

These figures make the trade-off clear. No-medical coverage can be valuable when needed, but it rarely wins on price alone.

Looking at life insurance quotes is a good way to get value in Canada. The prices of life insurance can be different from one insurance company to another, even if you have the same profile and the same policy details.

This is why it is important to look at and compare your choices, not just pick a company because you know the name. Canada Life might be the best deal for one person. But another insurance company could be better for someone else. The best thing to do is check that the products you look at are the same. Then you can judge the price and see which is the best fit for you.

You can find many life insurance quotes online by using comparison platforms or digital broker sites. These tools let you look at choices from more than one company, so you do not have to reach out to each one on your own.

This can help you save time and notice price differences fast. Policy Ninja is one place where people in Canada can see affordable life insurance quotes from many companies. You can also talk to a licensed advisor there if you need to. For a lot of people, getting life insurance online this way is simpler.

A good quote site should help you:

This is usually the best way to find the lowest price that fits.

First, look for clear quote details. The right platform should show things like the policy type, coverage options, term length, and the premiums. All of these should be easy to compare. If these details are not shown, then the cheapest price may not be what you think.

It also helps if the platform tells you if the quote is for a fully underwritten, simplified, or guaranteed issue coverage. This is important, because the type of life insurance product you get can change what you pay and what you get. People searching for universal life insurance or learning about whole life, or asking about term vs whole life insurance in Canada, really need these details kept simple.

Helpful comparison features include:

Good online platforms for life insurance can help a lot. They make sure you get both speed and clear info.

Sample policies can help you see more than just the headline price. Before you buy life insurance, read the details to find out how the plan works. Look for things that are not covered, and see if the plan fits what you want.

Check the term length and if you can keep your plan or change it later. Be sure to know if you are getting regular life insurance or an issue life insurance. If it is simplified or guaranteed issue, see if there is a time you have to wait before you get covered, and watch for lower coverage limits.

Focus on these points when you review:

Doing this can help you not make the mistakes other Canadians make when they chase just the cheapest price.

Talk to a licensed advisor when your needs are not simple or when you do not feel sure about the quotes you see. This is important if you have kids, a lot of debt, health problems, or you wonder if term or permanent coverage is better for you.

An advisor can also help you when you need to compare your personal needs and business needs. Some searches, like what is key person insurance, executive life insurance Canada, corporate owned life insurance Canada, buy sell life insurance Canada, buy sell agreement insurance Canada, how does buy sell insurance work, partnership life insurance Canada, shareholder protection insurance Canada, business succession insurance Canada, business continuation insurance Canada, business overhead expense insurance, and business insurance advisor Canada often need advice just for your situation.

You may want to ask for help from an advisor if:

Saving money on life insurance is all about timing, picking the right plan, and smart shopping. You will find the best savings if you apply early. It helps when you pick a good term. Try not to pick options that are too expensive if you do not need them.

To get lower premiums, go for full underwriting when you can. Keep your coverage close to what you really need, and see if yearly payment discounts will work for you. The goal is not always to get the lowest cost. It is about making sure you have strong life insurance that you can pay for over time, and that you get it from the right company.

Getting a life insurance policy when you are young and in good health can save you a lot of money. The lowest premiums are often given to young people. This means getting a term life or life insurance policy can be cheaper. It can also give you better coverage. Once you start facing health conditions, you will see your insurance rates go up. So it helps to make this choice early. Looking at different term life insurance plans now can give your family the financial protection they need.

If you act early, your premiums will likely be lower. You can get a policy that covers what you may need in the future. It also helps to get quotes from a few companies, like PolicyNinja, so you find what works best for you.

Sticking with the important parts of life insurance helps you get the safety you need without paying too much. Many life insurance policies have extra features that can make the price go up, but they may not give you much more peace of mind. If you choose simple options, like term life insurance or basic whole life plans, you can still get good coverage and pay less. Focusing on what matters in your policy lets you plan your money better. This means you have more to put towards other things you want or need.

If you want help picking the right life insurance for you, checking different choices at PolicyNinja can help you find a plan that is good for your wallet and gives the security you and your family need.

Keeping up with good health helps you get lower premiums on your life insurance policy. During the application process, insurers look at your health condition. If you are in good health, you can get insurance rates that are much lower. Going for regular check-ups, eating a balanced diet, and having an active lifestyle not only make you feel better, but they also let you get better coverage options at good prices.

If you worry that your premiums may go up, taking care of your health can help with this. Talk to your doctor, learn about your family history, and work on any chronic conditions. These steps make it easier to keep life insurance policy costs down and affordable for you.

Paying each year for your life insurance can help you spend less in the long run. Many companies give you a discount if you pay all at once instead of each month. This saves you money on interest charges and fees. When you pay for the year, it helps you plan better for your money. You also get the best price you can. It keeps your life insurance from being at risk if you forget a payment in a month. With yearly payments, the policy will not get cut off because of missed deals during the month. Take some time to look at quotes on PolicyNinja so you can find good prices. This lets you make a good choice for both your money and the coverage you need.

Looking for affordable life insurance can lead people to make some common mistakes in Canada. One big mistake is getting too little life insurance just to get a lower price, but this can leave your family with not enough help. Some also miss out on important parts of their policy, like extra choices that cover serious sickness or pay out if someone passes in an accident. You may think what you get from your work is enough life insurance.

Most of the time, it is not good for your whole financial needs. A lot of people also do not check their policy as their life changes, so they lose the chance to change it or deal with new health problems. If you know about these mistakes and do not make them, it can help you get the right life insurance for your needs.

Choosing the plans with the lowest premiums can show up as big problems later. You could be left with an insurance policy that lets your loved ones down. A life insurance policy that looks good because it is cheap may not give enough for your family’s needs in the long run. It is important to know your own money responsibilities, like final expenses or your children’s education. You need to be sure that the coverage amount will help your family stay safe in the future.

To get a life insurance policy that works for you, try to balance cost with what coverage you really need. Look at quotes from different companies. This lets you see what each life insurance plan gives you. You can use PolicyNinja, too, to find life insurance choices that fit your budget, give you good coverage amount, and cover everything important so nothing is missed.

Missing important riders in a life insurance policy can create big gaps in what you get if something happens. Riders are add-ons for your policy. They boost your insurance and give you more help, like covering you for a critical illness or letting you skip payments if you can’t work from a disability. These extras can give you and your family peace of mind if life takes a turn.

Buying a life insurance policy without these riders may look cheaper at first. But if you need more coverage later, you might end up paying more out of your own pocket. It’s good to look at your financial needs and think about what your family needs right now and in the future. That way, you can get the insurance policy and riders that suit you best. For more help comparing riders and features, you can check out options at PolicyNinja.

Relying only on what your work gives you for coverage can leave you open to problems with your financial security. A lot of work plans give small benefits and may not cover what your family will need for a long time. That is why it is good to look at your own life insurance plans on top of any group plan you get from work. Employer coverage often stops if you leave your job. This can leave you and your family without enough safety. It helps to look into term life or term life insurance because this kind of plan can give a strong safety net. To truly cover your family's financial needs, get affordable life insurance on top of what you get at work. You can look at different life insurance choices and compare quotes at PolicyNinja to find one that fits you and your family's needs.

Life insurance needs to change as your life changes. Things like getting married, having kids, or buying a new house can make you have more bills to pay. If you don't check your insurance policy often, you might not have enough coverage. This can make it hard to keep your financial security in place. When you look at how much coverage you have, you can see if your life insurance matches what you need now.

If you update your insurance policy often, you might find ways to get lower premiums or change the benefits. It is good to make sure your life insurance fits your life as it changes. This will give you peace of mind and help keep you safe from any big problems with your money when you need insurance the most.

The best way to choose a good life insurance policy is to find trustworthy insurance companies. This helps you get the protection you need and avoid paying too much. Start by checking different life insurance options. Look at their financial stability and see how well they treat their customers. You want to be with a company that gets good reviews and is well-known in Canada.

You can also talk to a life insurance broker near you. They will know what is best for you and can give advice fit for your needs. It helps to use a platform like PolicyNinja. They compare many insurance policies for you so you find ones that are good and fit your budget.

Find the right life insurance easily at policyninja.co.

Several well-known life insurance companies in Canada have many different products to match your financial needs. Some top insurance companies you might know are Sun Life, Manulife, and Canada Life. Each of these offers many choices, like term life and permanent coverage. These life insurance companies have a good name because of their financial stability and customer service. You can trust them to help you with your life insurance and help you decide what works best for you.

When you look for a provider, you may want to check customer reviews and see how well they handle claims. If you want to make the whole process easy, you can use websites like PolicyNinja. This can help you compare different insurance companies in less time. You can also get advice that fits your needs and look at different rates to find what will work best for you.

Finding an insurer with good financial stability means you need to check a few things. First, look at ratings from independent groups like A.M. Best or Standard & Poor’s. These ratings help you know if the company is strong with money and can pay claims when you need it. You should also see if the company has a good track record with paying claims on time. This shows they are reliable.

It’s a good idea to check what kinds of insurance products they have. You may want to look into their customer service, too. This helps you know you will get help if you ever need it.

If you want to compare many options, you can go to PolicyNinja. There, you can see quotes from many different providers and find the one that fits you best.

Feedback from other customers can help you know if a life insurance company is good and reliable. When people share good reviews, they often talk about great customer service. This can give you peace of mind. You feel sure your claims will be handled well. Bad reviews, on the other hand, might show bigger problems at a company. These can be a warning for you.

A good insurer will care about customer happiness. They will answer your questions in a timely way and be clear about what they offer. By looking at what other people say, you can choose from the best life insurance options. You are more likely to find affordable life insurance this way. This will give you peace of mind and help you protect your future.

Compare quotes at policyninja.co for the best deals.

When you look at online sites like PolicyNinja, it’s important to see how open they are, what other people say about them, and how they help you as a customer. Good sites will show you clear details about the plans they offer. They should also have a solid financial base and be quick to help when you reach out. Always take some time to check them out and make sure they fit what you want in your insurance.

When you pick the right life insurance, you need to guess how much life insurance your family will need. It helps to think about how much you have to pay. The plan should still give your family the coverage amount to protect them. Talk with your spouse or partner about the choices. This way, you both get to share what you think, and you will make better choices together.

If you add kids to your plan, it can give you peace of mind. This helps you feel better about money that is needed for things like school and other care for your children. It is good to change the coverage amount as your life changes. Keep checking what you have.

Look at different quotes when you want to explore life insurance. With PolicyNinja, you can find good and affordable options. They help you reach dependable companies. This lets you choose what fits best for your family’s needs.

Choosing the right life insurance for your family means looking at your needs and your money situation. You want to find an insurance policy that gives enough financial protection for your family without making you spend more than you can handle. Think about things like any debts you have, how much you will need for your kids’ school in the future, and the cost of any final expenses.

Getting life insurance quotes that match your situation can help you see what coverage amount is best for you. Make sure the life insurance policy you pick will help with your family’s financial stability over time. You can use sites like PolicyNinja to look at many affordable choices from many insurance companies. This makes it easier to find the coverage that is the best fit for you and your family.

Finding the right mix of price and protection with life insurance is important. It helps you keep your money safe for the future. Many people go with a term life insurance policy. This is because a term life option often has lower premiums than whole life plans. There are some things that can change your life insurance rates. These include your age, health, if you smoke, and your coverage amount.

It is also important to know your own financial needs. Do not just pick a policy with the lowest cost, as you could get less protection than you need. When you want to compare life insurance policy quotes, or if you want the best advice for choosing coverage, check out PolicyNinja. The site connects you to licensed advisors. They can help you get the best life insurance for you.

It’s important to talk with your partner or spouse about life insurance. This helps make sure you both get the right financial protection for your future. You both need to look at what you owe now, like your children’s education costs and any final expenses. By talking about how much coverage you need and picking the right life insurance policy together, you build trust. You both stay clear about your money goals.

It’s smart to try a life insurance calculator. It helps you figure out how much coverage will be good for your family and what you like. Together, you can check out many life insurance options and find one at a good rate. This way, you get the best life insurance for your needs. For advice made just for you, you can get quotes at policyninja.co.

When you want to get coverage for your children, think about what they will need later and how sudden problems may affect the family money. Find policies that give the most needed benefits, but do not pay for too many extras you do not want. Be sure the coverage is right for your family and fits your budget.

The way you pick life insurance can be different at each stage of your life. The right fit often depends on where you are now. If you are a young adult just getting started, term life insurance can give you good protection for less money. The lower premiums can help you save money at this time.

When you have children or a family, you should look at how much coverage you will need to meet all the needs of your loved ones. This means thinking about things like your children’s education or covering final expenses. These can give you peace of mind, knowing that your family will be okay, no matter what happens.

As you get nearer to retirement, it could be a good time to look into permanent life insurance. This type of coverage can help with estate planning and also help you keep financial stability as plans change over the years.

Make sure you look at your coverage options every now and then to keep up with your changing financial needs. If you want help finding the best choice for you, you can visit PolicyNinja. It is a helpful way to find affordable, easy options that fit what you need now.

Finding the right plan can seem hard for students and young workers, but it does not have to be. Term life insurance is a good choice for many people. It gives you coverage at lower premiums than a whole life plan. Some things that change how much you pay are your age, your health, and if you smoke or not. If you want to save money, stay in good health and pick a standard plan. These can make costs go down. It is a good idea to check quotes from more than one company. PolicyNinja helps you compare options and find affordable life insurance or term life insurance that works for your needs.

Making a budget for a growing family means you have to handle both daily costs and plan for the future. Having enough life insurance coverage is important. It helps give you financial security and peace of mind. When children get older, your insurance needs may change. So, it is important to look over your coverage options now and then to be sure your loved ones are protected, but that you don’t spend too much.

Using term life insurance can be a good and low-cost way for young families to make sure they have a strong financial future. You can look at quotes from different insurance companies to find good prices for your premiums. Not picking extra features that you do not need makes it easy to get the coverage that matters and still help keep your monthly costs under control. Go to PolicyNinja if you want to compare numbers, check options, and make smart choices for your family’s future.

As you get close to retirement, the need to check your life insurance coverage is big. Many people may lower their life insurance policy needs, but you want to make sure your family still has help with money if something happens. The aim is to choose the right coverage amount that keeps insurance affordable. This protects the people you care about and helps you avoid paying for more insurance than you need.

You may want to switch from a term life insurance policy to whole life or universal life insurance, as these can give you lifetime coverage and can build cash value. Making this kind of change could help you stay safe with money through the years without spending too much. It is smart to check your life insurance plans often as you get older. This way, you can adjust the insurance coverage or premiums. Then you will have the life insurance coverage you need and can make the most out of your plan.

Getting life insurance can be easy when you use PolicyNinja. On this website, you can compare quotes from many Canadian providers. This helps you get coverage that fits your needs and is not too expensive. The application process is simple. It leads you through each step, like any health conditions you have and the coverage amount you want.

Customer service is important at PolicyNinja. You can talk to licensed advisors if you need help. They will explain the difference between term life and whole life insurance, so you get the best plan for you. See different coverage options and give your family better financial security by looking at affordable quotes at policyninja.co.

Getting life insurance quotes can feel tricky, but PolicyNinja makes it simple. You just put in your details, and you can see the different policies out there from many Canadian insurance companies. This helps you get the right coverage at a good price. There are many options for you, including term life, whole life, or even permanent insurance. As you go through the application process, there are licensed advisors who can help answer any questions and walk you through each step. If you want an easy way to look at your choices, save money, and have peace of mind, check out policyninja.co now to compare good, affordable life insurance quotes.

Choosing the right life insurance can be hard, but a PolicyNinja advisor makes it easy. These experts have a lot of knowledge about different insurance companies and products. They help you pick coverage that fits your financial needs. They also work with you during the application process. The advisor will make sure all your medical questions are answered, as these can affect your insurance premiums.

One of the best things they do is compare quotes from many Canadian life insurance companies. This helps you find options that are good for you and your budget without losing quality. For help that is just for you, visit policyninja.co and connect with an advisor now.

Finding the right life insurance policy for you can feel hard. There are many choices out there. Working with an advisor makes this easier. You get advice made for your needs, so you get the life insurance that fits you best at a good price. If you want term life insurance or you are looking at other kinds, an expert can help. They will explain the terms and show you which insurance policy may work for you.

At PolicyNinja, there are licensed advisors who know about the Canadian life insurance market. They will help you every step of the way. They will also guide you through the application process. If you want the best term life policy or are looking for more about insurance policies in Canada, they can give real help.

Do not wait to find quotes that are easy to pay for. Get the advice you want now at policyninja.co.

Getting the right affordable life insurance coverage is important. You want to help protect your loved ones from money problems. Learning about different choices lets you find a good fit between what you pay and what you get. It helps you see the difference between term life or whole life insurance. Think about what you need from a policy—not just how low the monthly cost may be.

Looking at options with a trusted site like PolicyNinja lets you compare quotes from many Canadian companies. This way, you can make the process simple for you and your family members. Start by thinking about what kind of life insurance coverage you need now, so you have a safer future. If you want help that is made for you, go to policyninja.co.

Yes, you can get cheap life insurance in Canada without going through medical exams. Many insurance companies have simplified issue policies or guaranteed acceptance plans. These options ask only a few health questions and do not need full exams. This makes life insurance easier to get for people who want a low price. It is always good to get quotes from a few companies so you can find the best deal.

Affordable life insurance often covers most things that can lead to someone passing away. But there are some things that the policy may not pay out for. These often are if a person dies from suicide in the first few years, takes part in crime, or does very risky things. To know what life insurance really covers, always read their policy and know what is not included.

To know if your life insurance premium is good, check it against the average rates from more than one company. Think about things like your age, your health, and the coverage amount you want. You can use online tools to make these checks. This will help you get a competitive rate for your life insurance.

Cindy David, CFP, CLU, FEA, TEP, is President & Estate Planning Advisor at Cindy David Financial Group Ltd. in Vancouver. A recognized leader in wealth management and estate planning, Cindy guides clients with strategic, tax-effective solutions while championing innovation and women’s leadership in the financial industry. She is the former Chair of the Conference for Advanced Life Underwriting (CALU) — Canada’s professional association for senior life insurance and financial advisors that advances education, advocacy, and best practices in advanced planning and public policy.